SIGN has been under heavy selling by its ex-substantial shareholder, HSC Healthcare SB (HSC), especially throughout April. However, I view this a test to see the true strength of the share and market interest and the result is that SIGN's share price is still resilient with slight upward-bias throughout the month. HSC has on 14 APR cased to be a substantial shareholder after selling 3.5m shares on the same day. I believe the trend will go on where HSC will continue to sell the remaining 4m + share in the coming week riding on the high buying interest as witnessed from the resilient share price and high volume. It is high possible that HSC may eventually sell all the remaining shares before end of next week. After that, supply of SIGN share will become limited and this could possibly start driving the share price if the demand is sustainable.

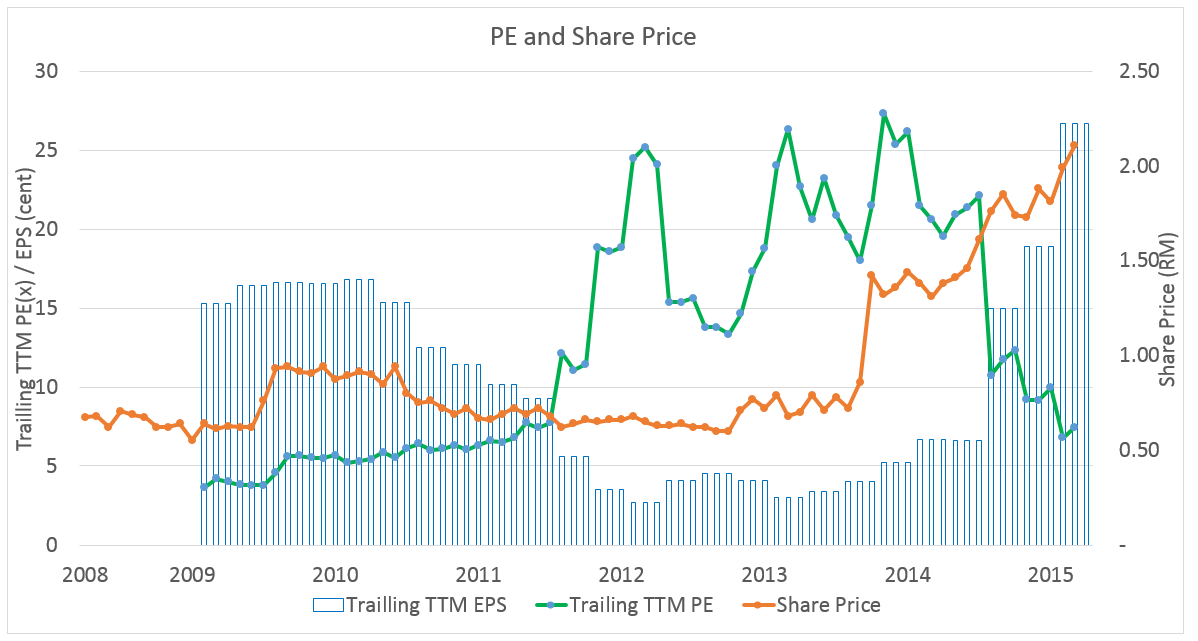

Hence, I reiterate my Buy rating on SIGN based on 1) current cheap forward valuation at 6.3x FY16's EPS based on optimistic earning growth projection 2) expected end of HSC's selling 3) CIMB Investment Bank's recent regional promotion on Small Cap Counters

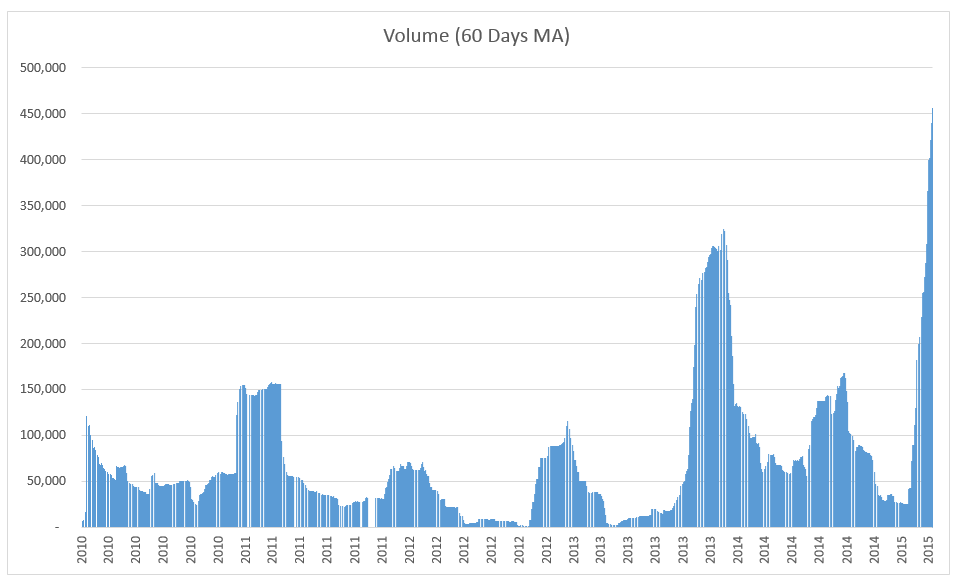

Diminishing Market Supply

|

| Chart from ChartNexus software |

HSC may finally dispose all their shareholding soon.

HSC's disposal has been the major supply of share in the market for the past 1 week. Yet share price still surged at 2.7% indicating strong market demand. If this trend persist, supply from HSC should be ended by next week.

Rising Demand due to

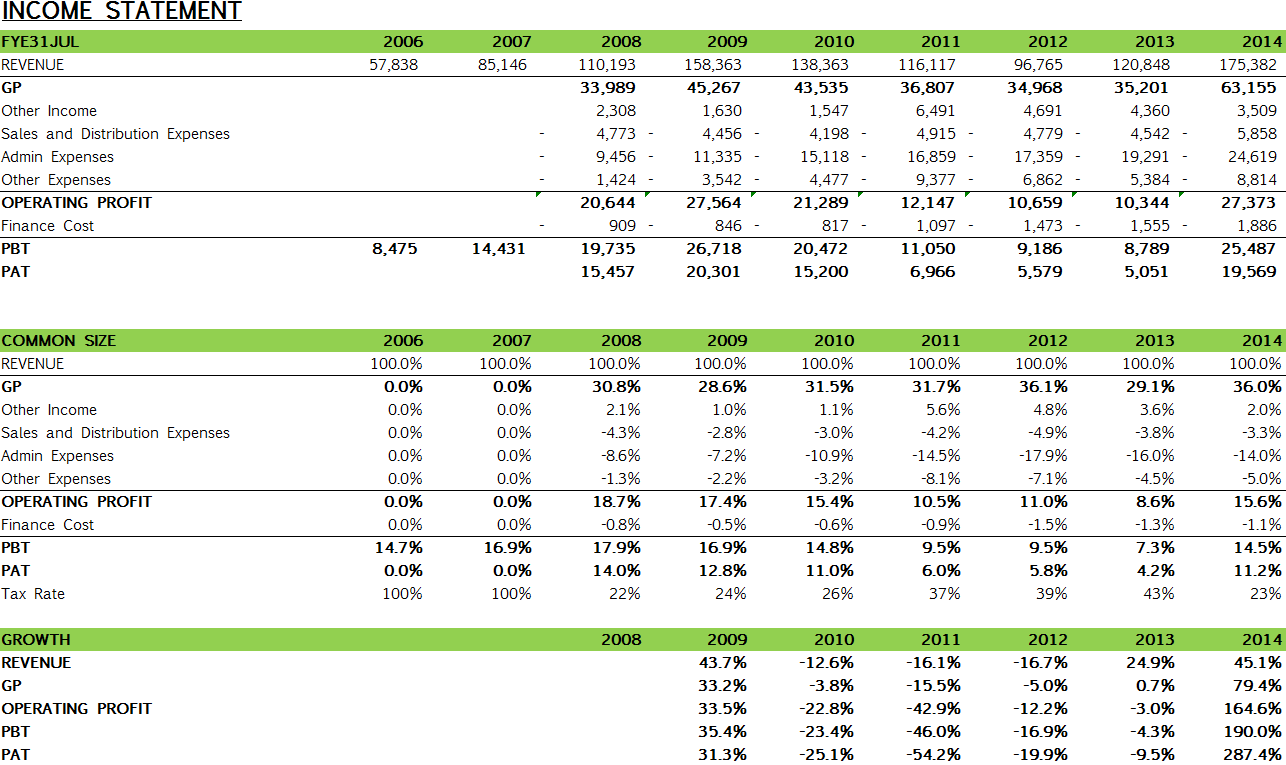

Cheap forward valuation and strong growth ahead

As per my previous recommendation

CIMB IB's Promotion of Small Cap Counter

In a Strategy Flash Note publised on 13 Apr 2015, Nigel Foo, analyst of CIMB IB mentioned that they have been marketing smallcap stocks in Singapore, HK and KL since early of Apr. They have met 74 fund managers (FM) from 32 institutions. The note mentioned that interest in smallcaps was strong in Singapore and KL. As SIGN is one of their highlights at the promotional activities, together with other stocks like OWG, IFCAMSC and others, I believe this effort have created awareness and possibly interest among FMs, though how it has generated the actual buying is not known.

Valuation

My TP remain at RM3.70 based on 10x FY16 EPS, which have not include SIGN's investment properties and their factory in Kota Damansara. CIMB IB has estimated the KD land alone is worth RM95m (RM0.79/share) based on RM300psf. Besides the KD factory, Together with their investment properties with Book Value of RM31m (as per 2014 Annual Report), this could increase SIGN's total value by RM1.05 per share.

Risk

HSC's disposal is based on pessimistic outlook or possessing of insider knowledge

However, HSC is only a shareholder but not involved in the day to day operation. Thus possibility of possession of insider knowledge is not high. The exit looks more like a earlier-planned action as Dr Lim Yin Chow, an ex-Non-Independent Non-Executive Director of SIGN who also has shareholding in HSC has resigned on 10 Jan 2014, much earlier than HSC's disposal. In conclusion, that is no material evidence supporting this risk, this make it a mere speculative concern.

Other Business Operation Risk

As per my previous post

{kind=link}

{kind=link}